Build vs. Buy vs. Partner: The Real Decision for Enterprise Web Security

An honest decision framework for in-house vs. licensed vs. operated security, and why 2026 changed the math behind all three.

Every few quarters, a version of the same meeting happens. Security has grown from a checkbox into a line item nobody can ignore, the board has started asking who actually owns it, and someone frames the decision as a clean fork in the road: do we build this ourselves, or do we buy it? It sounds like the whole question. It isn’t even half of it.

The build-versus-buy framing quietly assumes that “buy” means you’ve solved the problem, when all it means is you’ve acquired a tool. The option it leaves out is the one most enterprises actually fall into, usually by accident and rarely on purpose: a capable platform that nobody is really running. Licensed, deployed, and then left to drift while the team that was supposed to operate it gets pulled onto the next fire. The real decision has three doors, not two. You can build it, you can buy it and run it yourself, or you can partner with someone who operates it for you. Each comes with a different cost, a different level of control, and a different answer to the only question the board will eventually ask: when something goes wrong at 3 a.m., who is awake and accountable?

What makes this worth revisiting in 2026, rather than reaching for the same spreadsheet you used three years ago, is that the ground has moved under all three options. The talent math hasn’t improved. Attacks now arrive at a scale and speed no human rota can react to. AI is rewriting the economics of a security operations center from both directions at once. And a wave of regulation has made one thing legally explicit that used to be a matter of taste: you can outsource the work, but you cannot outsource the responsibility. So the honest version of this post isn’t a pitch for any one model. It’s a framework for working out which of the three is right for you, and being clear-eyed about what each one really costs.

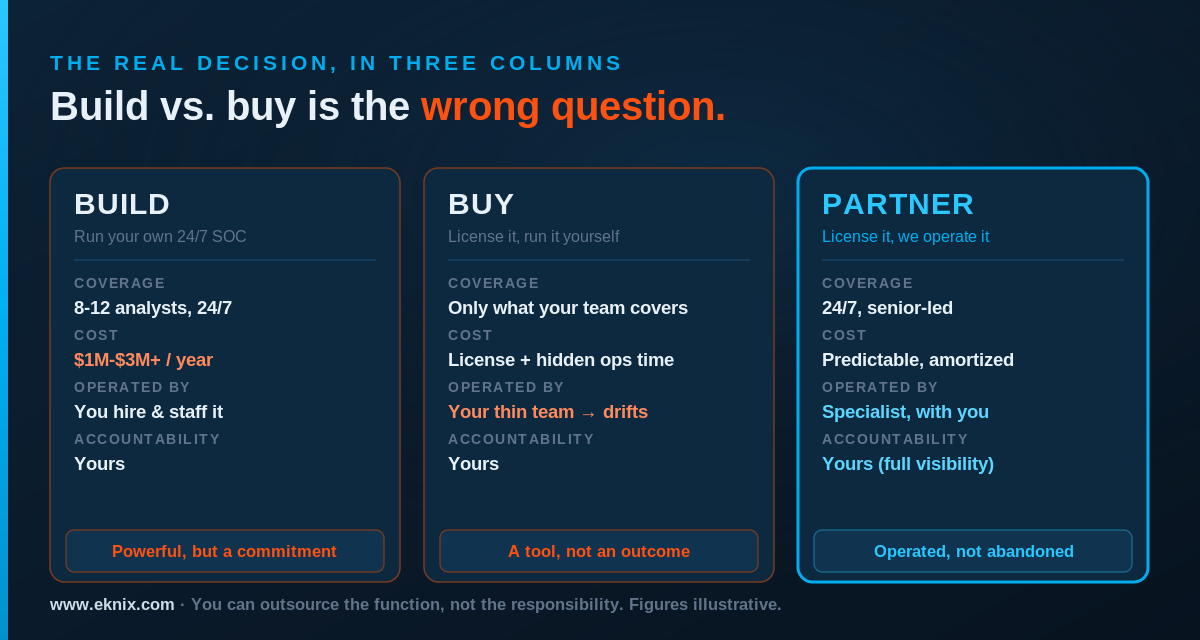

The short version: “Build vs. buy” is the wrong question, because “buy” usually delivers a tool, not an outcome. The real choice is build (run your own 24/7 SOC), buy (license a platform and operate it in-house), or partner (license it and have a specialist operate it for you). Building demands 8 to 12 analysts for genuine round-the-clock coverage and a budget that starts north of a million dollars a year, in a market where the skills gap never closed. Buying-and-self-running fails in a specific, common way: tools without operators drift, alerts pile up, and the platform you paid for slowly stops protecting you. Partnering wins in the band between those two, but only with a real operator, not a reseller who deploys and disappears. Three things make 2026 different: the AI SOC is changing the cost of operations, the 31.4 Tbps DDoS era has made always-on edge defense a baseline rather than a luxury, and NIS2 and DORA now pin accountability personally on your leadership no matter who runs the stack. Match the model to your size, maturity, and regulatory exposure, and watch for the red flags in each.

Three models, not two

Before the matrix, the definitions, because most of the confusion in these conversations comes from people using the same words to mean different things.

Build means you own the whole thing. You hire the engineers, you stand up the security operations center, you select and integrate the tools, you write the runbooks, and you staff the rota that watches the dashboards at the weekend. You carry the capability internally, end to end. At full maturity this is the most powerful option and, done well, the most tailored to your environment. It is also the most expensive and the hardest to sustain, and the place where good intentions most often outrun the budget.

Buy means you license a capable platform, a web application firewall, a bot manager, DDoS protection, an API security layer, and you run it yourself. This is the option that gets mislabeled as “solved.” Buying a powerful platform gets you the engine. It does not get you the driver. Someone on your team still has to tune it to your traffic, separate the real alerts from the noise, respond when it fires, and keep it calibrated as your application changes underneath it. Buy the tool, keep the operating burden.

Partner means you license that same platform and bring in a specialist to operate it with you. The good version of this is not a reseller adding a margin to a license and walking away. It’s a team that takes operational responsibility (monitoring, tuning, incident response, reporting) while you keep full ownership and visibility of your own environment. The whole value is in the verb. As we put it on our own about page, the failure mode to avoid is “a generalist partner who deploys and disappears.” A partner worth the name operates; a reseller transacts.

Those are three genuinely different businesses to be in. The mistake is treating the middle one as the safe default, paying for the platform, and discovering eighteen months later that you bought a Formula 1 car and parked it.

What “build” really costs in 2026

Building your own security capability is the right answer for some organizations. It is almost never the cheap answer, and the gap between the budget and the reality is widest on the part nobody costs properly: the people.

Start with coverage. Attacks don’t keep office hours; the worst of them deliberately land overnight and at the weekend, when the in-house rota is thinnest. Genuine 24/7/365 monitoring with a single seat always covered, once you account for shifts, holidays, sick leave, training, and the attrition that plagues this field, realistically needs somewhere between eight and twelve analysts. That’s before you’ve hired the architects who design the thing or the engineers who keep the tooling integrated. Industry build-versus-buy analyses put the all-in annual cost of a functioning in-house SOC in the range of one to three million dollars and up, with a loaded senior analyst running well into six figures. Treat those numbers as directional, since they mostly come from vendors with a horse in the race, but the staffing arithmetic underneath them is not controversial. Round-the-clock coverage is expensive because round-the-clock is a lot of clock.

Then there’s the question of whether you can hire the people at all. The cybersecurity workforce shortfall hit a record 4.8 million unfilled roles globally in 2024, according to ISC2. Telling, in its 2025 study ISC2 stopped publishing a single headline gap number and reframed the problem around skills rather than headcount: a third of organizations said they don’t have the resources to staff their teams adequately, 29% said they can’t afford the skills they need, and the overwhelming majority reported a real security consequence from the shortfall in the past year. The constraint shifted from “the talent doesn’t exist” to “we can’t fund or retain it,” which is, if anything, a harder problem for a single company to solve on its own.

Even teams that clear the hiring bar hit the operating wall. A modern enterprise runs, on average, 83 security tools from 29 different vendors, according to IBM and Palo Alto Networks research from early 2025. Each of those generates events, and the volume long ago passed what humans can triage by hand. The 2025 SANS Detection and Response Survey found that 73% of security teams name false positives as their single biggest detection problem. When everything pages, nothing pages: the real incident sits in a queue behind four hundred that didn’t matter, and the analyst who’d have caught it is busy clearing the queue. This is the failure mode that costs you whether or not you ever get breached, and it’s structural, not a sign of a bad team.

Building, in other words, is a standing commitment, not a project. It can absolutely be the right one. But it asks for headcount you may not be able to hire, a budget that recurs every year, and an appetite for running an operation that is not your core business. Go in knowing that, or don’t go in.

Why “buy” quietly fails: tools without operators drift

If building is the option people underestimate the cost of, buying is the option people overestimate the completeness of. The phrase that captures the whole problem, and one we use on our own managed services page, is simple: tools without operators drift.

A security platform is not an appliance you install and forget. It’s a system that has to be continuously calibrated to an application that’s constantly changing. The bot rules that fit your traffic in January are subtly wrong by June, after three product launches and a marketing campaign that doubled your legitimate automated traffic. The WAF tuned to last quarter’s API now blocks a partner integration and waves through something it shouldn’t. A firewall on default rules, as we argued at length in why default WAF rules aren’t enough for fintech, is a starting line dressed up as a finish line. The work is never done because the thing it protects never stops moving.

This is also where the most expensive in-house initiatives stall, not at deployment, but just after it. We’ve watched it happen often enough to write a whole piece on why most microsegmentation projects stall, and the pattern generalizes to almost any security platform: the rollout gets funded and celebrated, the operating model doesn’t, and the capability decays in slow motion while everyone assumes someone else is watching it. Buying solves the question of which engine you have. It does nothing for the question of who’s driving, and the second question is the one that determines whether you’re actually protected.

The honest case for “buy and self-operate” is narrow but real. If you already have a mature, well-staffed security operations function with capacity to spare, licensing the best platform and running it yourself is exactly right; you get the tool and you already have the operators. The trap is buying as if you’re in that position when you’re not, which describes a great many organizations that have a capable platform, a thin team, and a quiet, growing gap between the two.

The 2026 wildcards that changed the math

The three-way decision has existed for years. What’s new is that three forces specific to 2026 have shifted the balance between the options, and any framework that ignores them is solving last year’s problem.

The AI SOC is rewriting operations economics on both sides

The most consequential change is that AI has arrived inside the security operations center itself. Gartner expects 40% of enterprise applications to feature task-specific AI agents by the end of 2026, up from less than 5% in 2025, and security operations is one of the clearest places that’s landing. AI is taking over the first pass of alert triage, correlation, and investigation, the exact high-volume work that drowns human analysts, and compressing response times that used to be measured in tens of minutes.

It’s tempting to read that as “build just got cheaper, because AI replaces the analysts you couldn’t hire.” Be careful. The same Gartner that’s bullish on agents also predicts that more than 40% of agentic AI projects will be canceled by the end of 2027, undone by cost, weak risk controls, and unclear value. An AI SOC is not a thing you download. It’s a stack that has to be chosen, integrated, governed, and supervised by experienced people: the same scarce people the talent numbers say you can’t easily hire. AI changes what a security operation costs and what it can do, but it raises the bar on the expertise needed to run one well. For most organizations that pushes the advantage toward whoever can amortize that expertise across many environments, which is the structural argument for a partner, not against one.

The 31.4 Tbps era made always-on defense a baseline

In December 2025, Cloudflare reported mitigating a 31.4 Tbps DDoS attack from the Aisuru botnet, the largest ever publicly recorded. It lasted roughly 35 seconds. Read that twice. The biggest attack in history was over before a human could read the alert, let alone respond to it. Network-layer attacks roughly tripled over the year, from 11.4 million to 34.4 million in Cloudflare’s count, and hyper-volumetric bursts are now rentable by anyone with a grudge and a credit card.

This quietly settles part of the build-versus-buy debate by force. You cannot build 31 Tbps of absorption capacity in-house; almost nobody can. Akamai’s Prolexic platform advertises more than 20 Tbps of dedicated defense capacity across 32 global scrubbing centers, on a network that totals over a petabit per second, with a zero-second mitigation commitment because in a 35-second attack there is no second to spare. That scale is a thing you license, never a thing you stand up yourself. The interesting question is no longer whether to buy the capacity. It’s whether you have the people to operate it under fire, which loops straight back to the build-versus-partner choice for everything that sits on top of the raw pipe.

The attack surface itself moved to APIs and agents

The same shift we wrote about in preparing your stack for agentic shopping is widening the operating burden. Akamai’s 2026 research found API attacks up 113% year over year, with the average enterprise absorbing more than 250 API attacks a day, and APIs overtaking the front-end as the primary attack surface. Defending an estate that’s increasingly machine-to-machine, where benign automation and malicious automation look nearly identical, is more operationally demanding than guarding a website ever was. More surface, more nuance, more tuning, all of which raises the cost of the “operate it yourself” column relative to where it sat even two years ago.

The accountability you can’t outsource

Here is the part that trips up the lazy version of the partner pitch, and the reason the honest version is more persuasive. Partnering does not move the liability off your desk. In 2026, regulation has made that explicit.

For financial services in the EU, the Digital Operational Resilience Act (DORA) has been fully applicable since January 17, 2025. Its text is blunt about third parties: relying on an ICT provider “cannot reduce the responsibilities” of the financial entity, and the management body remains responsible for the risk-management framework no matter who operates the controls. The NIS2 directive goes further still for the broader set of essential and important entities it covers, putting cybersecurity oversight on management bodies personally and making that accountability something you cannot delegate to IT or sign away to a vendor. (Worth noting that NIS2 transposition across member states is still uneven in 2026, with the Commission pursuing several states that missed the deadline, but the direction of travel is not in doubt.)

What that means for this decision is precise and easy to miss. You can outsource the function. You cannot outsource the responsibility. So the question to ask any partner is not “will you take this off my hands?” but “will you operate it in a way I can see, audit, and answer for?” The wrong partner is a black box that leaves you accountable for a thing you can no longer inspect. The right one operates transparently (documented changes, named contacts, real reporting) precisely because they know the liability stays with you. It’s why our managed service keeps you with full access to your own platform rather than locking you out: as we tell every client, we operate as an extension of your team, not a gatekeeper. In a post-DORA, post-NIS2 world, a partner who makes your environment less visible is a liability dressed as a convenience.

A decision matrix by size and maturity

There’s no universal right answer, but there is a pattern, and it tracks two variables more than any others: how big and complex your estate is, and how mature your existing security operation already is. The table below is a starting point, not a verdict. Your regulatory exposure and risk appetite can move you a row in either direction.

| Profile | Estate & risk | In-house maturity | Usually the best fit | Why |

|---|---|---|---|---|

| Startup / small team | Small surface, low traffic, growing fast | None to minimal | Buy, lean on vendor defaults | Can’t justify a SOC; needs protection now. Acceptable as long as someone owns the basics. |

| Mid-market / scale-up | Real revenue online, real attacks, lean team | Some skills, no 24/7 | Partner | The classic gap: enough at stake to need real operations, not enough scale to staff them. The band where partnering wins clearly. |

| Enterprise, immature ops | Large, complex, regulated-ish | Tools bought, thinly run | Partner, then build selectively | Already in the “tools without operators” trap. A partner stops the drift while you decide what to bring in-house. |

| Enterprise, mature SOC | Large, complex, high-stakes | Well-staffed 24/7 SOC | Build core, partner the edges | You have the operators. Build what’s differentiating; partner the specialist or always-on layers (edge DDoS, niche tooling) you’d be unwise to staff alone. |

| Regulated enterprise (finance, critical infra) | High value, DORA / NIS2 in scope | Varies | Partner or hybrid, with strict visibility | Accountability is non-negotiable and non-delegable. Whatever the model, demand auditable, transparent operations. |

The matrix’s real message is the diagonal. Almost nobody should be pure-build except the largest, most mature operations, and even they partner the edges. Almost nobody should be pure-buy-and-forget except the smallest, lowest-risk teams. The vast middle, the mid-market scale-up and the big-but-thinly-run enterprise, is where partnering does its most honest work, because it’s the band where the stakes have outrun the staffing.

Red flags in each model

Whichever door you pick, there are warning signs that you’ve picked it badly. These are the ones worth watching for.

If you’re building, the red flag is a deployment with no operating model attached. If the project plan ends at “go live” and there’s no named rota, no tuning cadence, no incident runbook, and no budget line for the people who’ll run it next year, you’re not building a capability. You’re buying a future drift problem with extra steps. The second red flag is a single point of human failure: one brilliant engineer who holds the whole thing in their head and whose resignation letter is also your incident report.

If you’re buying and self-running, the red flag is silence. A security platform that never seems to fire, never needs tuning, and generates a tidy weekly report nobody acts on is not protecting you; it’s idling. The other tell is alert volume going up and investigation rate going down, the quiet onset of the fatigue that turns a tool into shelfware while the license keeps renewing.

If you’re partnering, the red flags cluster around the difference between an operator and a reseller. Watch for a partner who can’t tell you who specifically will be on your account, who quotes “best-effort” instead of a contractual response SLA, who wants to lock you out of your own console rather than operate alongside you, or whose commercial incentive is a clean handover document rather than a system that keeps working. A reseller’s job is done at signature. An operator’s job is done at 3 a.m. when something fires and they’re already on it because they knew your environment before the alert did. If the conversation is all about the license and never about the operation, you’re talking to the wrong kind of partner.

So which one is you?

The point of all this isn’t to land everyone on “partner.” It’s to retire the false binary that made the decision look simpler than it is. Some organizations genuinely should build, and the largest and most mature ones do. Some should buy and run it themselves, and the ones with real operations to spare can. But far more organizations than will admit it are sitting in the unhappy middle, with a capable platform, a thin team, and a slowly widening gap between what they bought and what they operate, because they answered a two-way question when they were facing a three-way one.

Work it backward from the question the board will eventually ask, the one about who’s awake and accountable at 3 a.m. If the honest answer is “we have the people and the budget to run this every hour of every year,” build it, and build the operating model with the same seriousness as the deployment. If the answer is “we have a great team with room to take this on,” buy the best platform and run it. And if the answer is the one most companies arrive at when they’re being honest, “we need this operated by people who do it for a living, without losing sight of a thing we’re still accountable for,” then partner, and hold whoever you partner with to the standard of an operator, not a reseller.